By Chris Bruen

Chris Bruen Senior Director of Research, with primary responsibility for aiding in and expanding upon NMHC’s research in housing and economics. Chris holds a bachelor’s degree in Finance from The George Washington University and an M.S. in Economics from Johns Hopkins University. He can be reached at cbruen@nmhc.org.

Metros with Higher Levels of Deliveries Record Lower/Negative Rent Growth

The U.S. has already built more than 360,000 apartment units in 2023, according to data from the Census Bureau, exceeding the total number of units built in all of 2022 (359,100 units). At this pace, multifamily completions are set to reach their highest level since 1988.

This surge in new supply has corresponded to a sharp moderation in the growth of apartment rents. According to CoStar, effective annual same-store rent growth (which incorporates concessions) fell from a peak of 11.4% in 1Q 2022 to just 0.6% year over year in 3Q 2023.

In this Research Notes, we examine the relationship between new apartment construction and rent growth at the metro level, finding that apartment rents growth has, in fact, slowed in geographies that built a greater number of units.

Markets with Higher Rates of Delivery See Lower Rent Growth

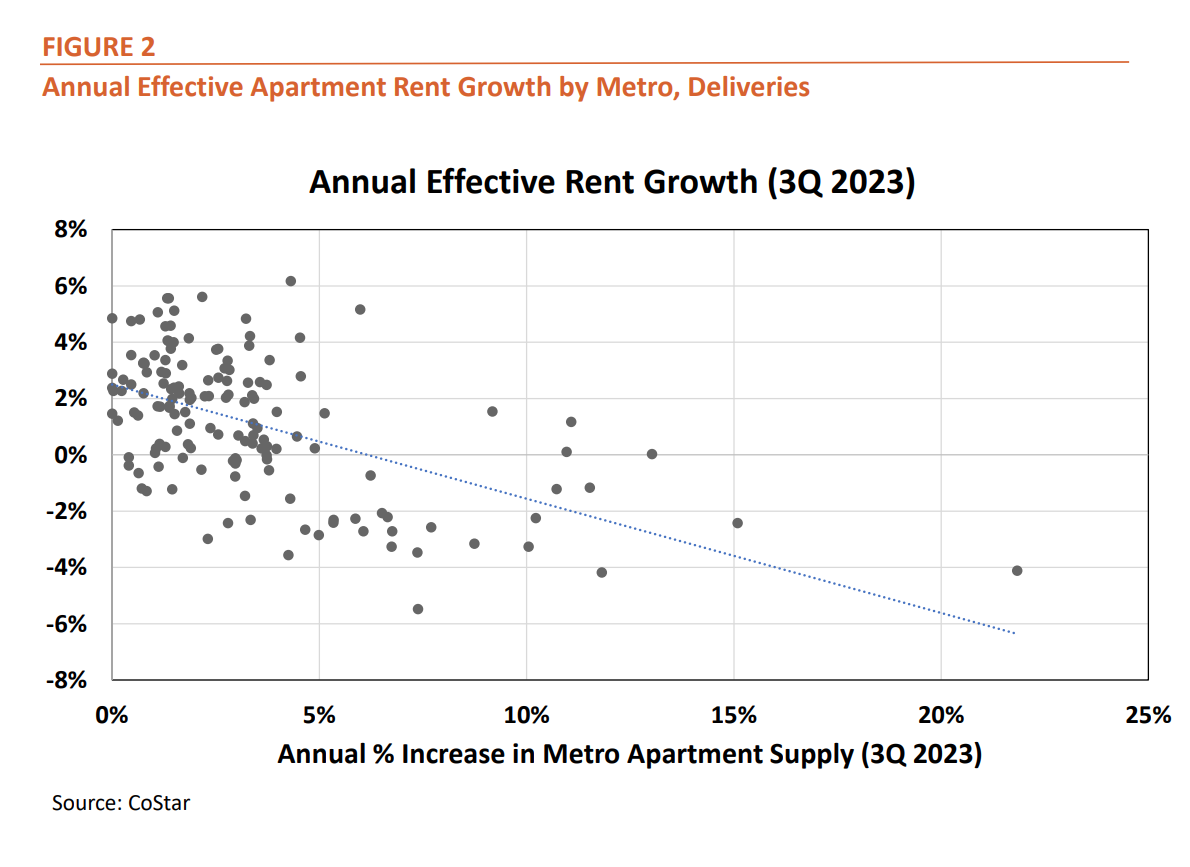

Looking at the largest 150 metro areas in the U.S. by apartment inventory, Myrtle Beach, South Carolina, recorded the highest rate of net annual apartment deliveries as of the third quarter of this year, expanding its apartment supply by 21.8%. Myrtle Beach also recorded a 4.1% annual decrease in effective apartment rents as of 3Q 2023, the second-lowest rent growth of all 150 metros (Austin, Texas saw apartment rents decrease 5.5% annually).

All but one of the top five metro areas by apartment deliveries recorded negative rent growth in the third quarter (rent growth in Provo, UT was flat). Of the 10 metro areas with the largest increases in their apartment supply, just three saw either flat or positive rent growth over this period.

Figure 2 above illustrates that there was in fact a strong negative correlation between apartment deliveries and rent growth. Specifically, we calculated a correlation coefficient of -0.54 between the two variables.

Furthermore, we found that higher levels of completions tended to correspond to lower levels of rent growth in both Class A and Class B apartments. Among metros where the apartment supply increased by 5% or more, 23 out of 26 recorded negative rent growth for class A units and 20 out of 26 saw negative rent growth for class B units.

Understanding the Relationship Between Absorptions and Rent Growth

We know, of course, that rent growth should depend not only on the supply of housing, but on demand as well. If new supply is accompanied by an equivalent increase in apartment demand, there should be no reason for rent growth to decrease.

Net absorption, or the change over time in the number of apartment units occupied, is frequently used as a measure of demand. Between 3Q 2022 and 3Q 2023, there was a 254,207 unit increase in the number of apartments leased in the U.S., according to data from CoStar, up from 212,093 units absorbed during the previous year but down significantly from the record 735,450 apartment units absorbed between 3Q 2020 and 3Q 2021.

While it may seem counterintuitive at first, we found that markets with a higher amount of apartment absorptions tended to have lower rent growth. However, higher absorptions also tended to correspond to higher rates of construction, which we’ve already shown are negatively correlated with rent growth. It makes sense that more apartments would be built in areas where there is more demand and, conversely, that leasing activity would be higher where more apartments are being built.

In order to isolate the separate impacts of apartment deliveries and absorptions on rent growth, we constructed a multivariate regression model, which found that:

- Higher absorptions, when separated from confounding supply effects, were associated with higher rent growth among CoStar’s top 150 metro areas. Specifically, a one percentage point increase in absorptions (as a % of metro inventory) was associated with a 61 basis-point increase in metro rent growth.

- Higher apartment deliveries were associated with lower rent growth among metro areas. A one percentage point increase in net deliveries (as a % of metro inventory) was associated with a 68 basis-point decrease in metro rent growth.

What these results tell us is that demand for apartments remains strong, and that even in markets with very high rates of construction, new deliveries are being leased up at a high rate. Yet, despite this robust demand, apartment owners in metros with higher rates of deliveries simply don’t have as much pricing power as those located in markets that have not built as much.

The Difference Between Absorptions and Demand

An important caveat to this analysis is that absorption numbers are a very imperfect measure of demand.

The number of apartments absorbed in a market depends not only on demand but also on the number of apartments available to rent. For instance, it would be impossible to rent an apartment in a market with 100% occupancy, but that doesn’t mean that there isn’t substantial demand to live there. Quite the opposite – an apartment market that is fully occupied is clearly one that has an excess of demand relative to the available supply.

In the real world, higher rents would likely prevent a market from ever reaching 100% occupancy during a housing shortage, but the effect on absorptions would be similar. Many people may want to live in a penthouse apartment in Manhattan, but such units are scarce and, thus, incredibly expensive, pricing out all but the wealthiest few. Again, absorptions for these units are low, but demand is exceptionally high.

We can, however, view the interaction of supply and demand through both the apartment vacancy rate and rent growth (higher demand relative to supply results in lower vacancy and higher rent growth and vice versa).

Conclusion

Annual apartment rent growth moderated from a record-high 11.4% in 1Q 2022 to just 0.6% in the third quarter of this year, according to data from CoStar.

Our analysis shows that this moderation can largely be attributed to higher levels of supply, with 2023 set to reach the highest rate of apartment completions since 1988. Specifically, we found that between 3Q 2022 and 3Q 2023, markets with a higher rate of apartment deliveries tended to have lower rates of rent growth, even after controlling for absorption. Those metros with the highest levels of construction even saw rents decrease over the past year.

However, the combination of this market softness and a rising cost of capital – NMHC’s Quarterly Survey of Apartment Market Conditions recorded decreasing availability of debt financing for nine consecutive quarters as of October – is already causing apartment construction to pull back.

- Multifamily permits (5+ units in structure) fell 3.2% to a SAAR of 486,300 in 3Q 2023, according to Census data, a 27.2% decrease from 3Q 2023.

- Starts (5+) dropped 23.4 percent in 3Q 2023 to a SAAR of 389,300, a 26.2 percent decline from the previous year.

Unless we find ways to remove more chronic barriers to supply, this balloon of apartment deliveries and reduction in costs is likely to be short lived, which will put upward pressure on rents and hurt housing affordability over the longer term.

About Research Notes: Published quarterly, Research Notes offers exclusive, in-depth analysis from NMHC's research team on topics of special interest to apartment industry professionals, from the demographics behind apartment demand to the effect of changing economic conditions on the multifamily industry.

Questions or comments on Research Notes should be directed to Chris Bruen, Sr. Director of Research, NMHC, at cbruen@nmhc.org.