Apartment operators face a tradeoff between the rents they set and occupancy. Higher rents can cause lower apartment occupancy rates, all else being equal, as some potential tenants seek cheaper accommodation elsewhere. Operators must decide, then, if an increase in rent is worth the cost of having more of their units sit vacant without collecting rent.

But how much vacancy do apartment operators tolerate, and how has this changed over time? Some have alleged that rising rents in recent years are a result of rental housing providers purposefully withholding units from the market and accepting a higher share of vacant units. However, the data tell a much different story overall.

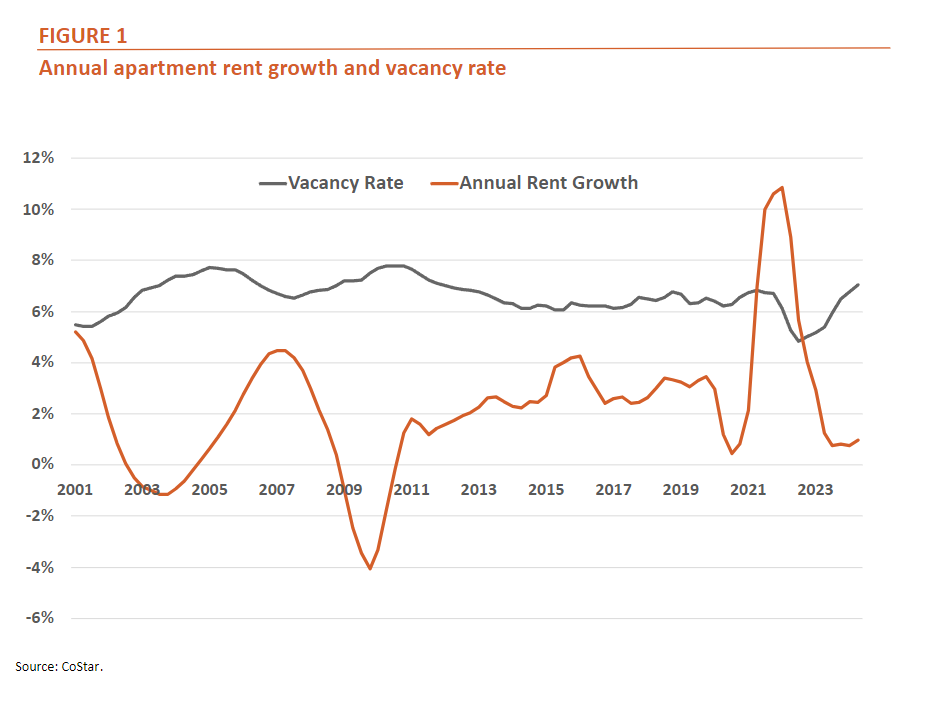

Significant apartment rent growth recorded in 2022 coincided with record-low vacancy rates

Apartment rent growth climbed to record highs in the first quarter of 2022, peaking at 10.8% according to CoStar. Yet, this elevated rent growth coincided with near record-low vacancy rates. The stabilized rental vacancy rate for apartments tracked by CoStar fell from 7.6% in 3Q 2009 to 4.3% in 1Q 2022 (up slightly from the record-low 4.0% reached in 3Q 2021).

This was not just a national trend either—of CoStar’s 150 largest apartment markets, all but four experienced a decrease in apartment vacancy between 3Q 2009 and 1Q 2022.

Vacant apartment units typically aren’t vacant for very long, especially during periods of high demand. In 2022, 17.2% of vacant rental units were already rented and just not yet occupied, while an additional 29.9% had only been vacant for less than one month at the time they were surveyed. [1] Just 6.9% of vacant rental apartment units had been vacant for a year or more at the time they were surveyed in 2022.

Increased deliveries have caused vacancy to tick up

And while apartment vacancy rates have since increased from their record lows – reaching 6% in 3Q 2024 according to CoStar—this can be attributed to a short-term surge in new supply. Multifamily completions rose 22.1% in 2023 to 438,500 units, according to data from the U.S. Census Bureau, the highest level since 1987. This pace of completions picked up even further to a seasonally adjusted annual rate (SAAR) of 561,300 during the first half of 2024.

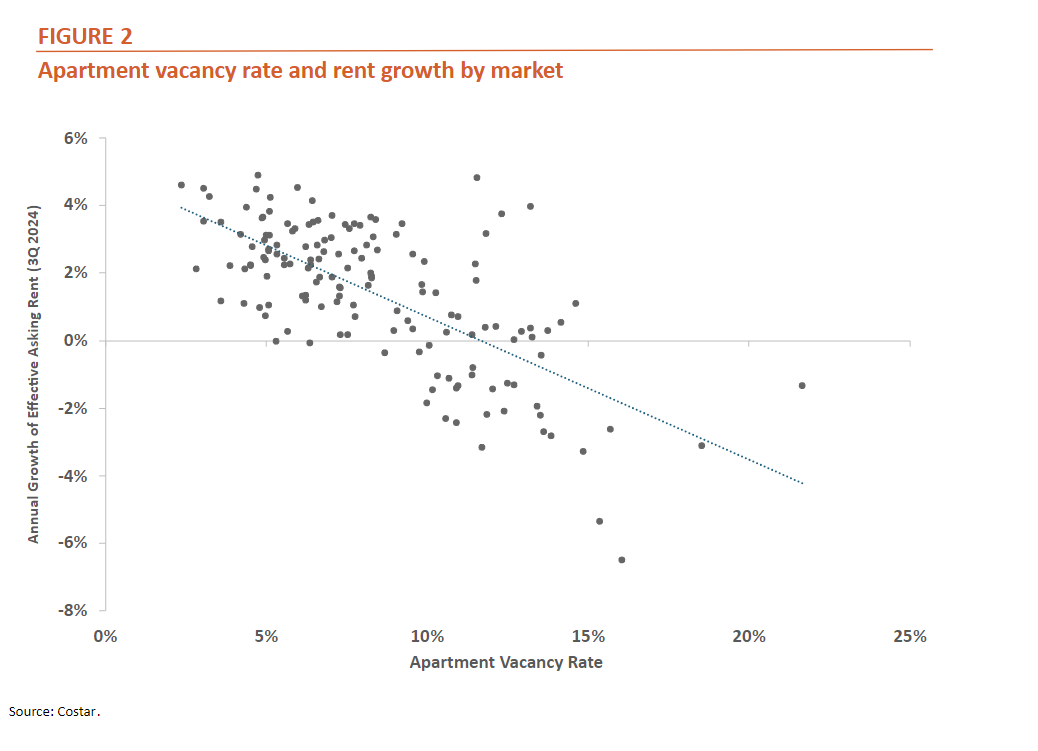

Moreover, despite this increase in vacancy, apartment owners are increasingly offering concessions and lower rents in an effort to lease their vacant units. Figure 2 below illustrates how markets with higher apartment vacancy rates in 2Q 2024 also tended to record lower (and often negative) rent growth.

This recent trend of increasing vacancy rates and moderating rent growth is likely to be short-lived, however, as a combination of higher interest rates, market softness and increasing operating costs (most notably, the cost of insurance and property taxes) have caused new construction to pull back significantly. Multifamily starts (5+ units in structure) were down 36.5% year over year as of 2Q 2024, according to data from the Census Bureau. Unless more is done to spur new development, this pullback in new multifamily residential construction will result in an increasing shortage of homes nationwide, characterized by decreasing vacancy rates and rising rents – similar to what we saw in 2021 and 2022.

[1] Tabulations of 2022 American Community Survey microdata.

About Chris Bruen

Chris Bruen is Senior Director of Research and Chief Economist, with primary responsibility for aiding in and expanding upon NMHC’s research in housing and economics. Prior to joining the Council, Chris conducted research on the behavioral tendencies exhibited by option traders and served as a contributor to the Shanghai-based business publication, MorningWhistle.com, where he wrote on topics relating to Sino-American economic policy. Chris holds a bachelor’s degree in Finance from The George Washington University and an M.S. in Economics from Johns Hopkins University.

Chris Bruen is Senior Director of Research and Chief Economist, with primary responsibility for aiding in and expanding upon NMHC’s research in housing and economics. Prior to joining the Council, Chris conducted research on the behavioral tendencies exhibited by option traders and served as a contributor to the Shanghai-based business publication, MorningWhistle.com, where he wrote on topics relating to Sino-American economic policy. Chris holds a bachelor’s degree in Finance from The George Washington University and an M.S. in Economics from Johns Hopkins University.

He can be reached at cbruen@nmhc.org.